library(tidyverse)

library(cmdstanr)

library(posterior)

library(patchwork)

source("00-utils.R")

kable <- knitr::kable

theme_set(theme_prodgray())

ols_erc <- function(.d){

fit <- lm(ret_dm ~ earn_surp_dm, data = .d)

fit_results <- broom::tidy(fit)

}

ols_pred <- function(.d){

fit <- lm(ret_dm ~ earn_surp_dm, data = .d)

fit_pred <- broom::augment(fit)

}

1. Introduction and preliminaries

This markdown file contains all the code necessary to replicate the main figures, models and results used in Section 3: Heterogeneity in earnings response coefficients of the Paper What Can Bayesian Inference Do for Accounting Research?. The prior predictive checks and the cross-validation test are on separate pages. All the code can also be found in the repo. It contains 00-utils.R which contains a few helper functions for graphs and tables.

Note: I used the newer cmdstanr package instead of the older rstan package because it likely is the future of the R based Stan ecosystem. I also really like its api, which is very close to the api of the pystan package. An additional advantage (I hope) is thus that most model fitting code should be more or less directly transferable to pystan for those that want to work in python. Installing cmdstanr used to be tricky at times because one needs a working c++ toolchain. But it is much smoother now. Please see the cmdstanr doc for installation instructions

2. Loading the data

2.1. Final transformations

The data used here is generated via the 02-create-ERC-sample.R script found in the repo. Here, we just load it and do some last minute transformations like de-meaning, etc.

ea_data <- arrow::read_parquet("../data/ea-event-returns.pqt")

ea_data <-

ea_data |>

mutate(

ret_dm = AbEvRet - mean(AbEvRet),

earn_surp_dm = earn_surp - mean(earn_surp)

)

head(ea_data) |>

kable()

| ticker | permno | fpend_date | ea_date | actual_eps | median_fcast_eps | num_forecasts | two_days_bef_ea | Price | earn_surp | ea_match_date | AbEvRet | firm_id | ret_dm | earn_surp_dm |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 001N | 14504 | 2014-12-31 | 2015-02-09 | 0.04 | 0.030 | 3 | 2015-02-05 | 14.49 | 0.0006901 | 2015-02-09 | -0.2428478 | 1 | -0.2472159 | 0.0006950 |

| 001N | 14504 | 2015-03-31 | 2015-05-05 | 0.06 | -0.045 | 4 | 2015-05-01 | 12.42 | 0.0084541 | 2015-05-05 | -0.0452097 | 1 | -0.0495779 | 0.0084589 |

| 001N | 14504 | 2015-06-30 | 2015-08-05 | 0.02 | -0.015 | 4 | 2015-08-03 | 9.25 | 0.0037838 | 2015-08-05 | 0.0469699 | 1 | 0.0426018 | 0.0037886 |

| 001N | 14504 | 2015-09-30 | 2015-11-04 | -0.02 | 0.040 | 5 | 2015-11-02 | 5.82 | -0.0103093 | 2015-11-04 | 0.0769411 | 1 | 0.0725729 | -0.0103044 |

| 002T | 14503 | 2014-06-30 | 2014-08-07 | 0.19 | 0.235 | 4 | 2014-08-05 | 33.33 | -0.0013501 | 2014-08-07 | -0.0166244 | 2 | -0.0209926 | -0.0013453 |

| 002T | 14503 | 2014-09-30 | 2014-11-04 | 0.18 | 0.340 | 5 | 2014-10-31 | 30.43 | -0.0052580 | 2014-11-04 | -0.0211484 | 2 | -0.0255165 | -0.0052531 |

ea_data_time <-

ea_data |>

mutate(EAYear = lubridate::year(ea_date)) |>

mutate(year_id = as.integer(EAYear - min(EAYear) + 1))

2.2. Tab. 1, Panel A.

desc_tabl <- rbind(

desc_row(ea_data$AbEvRet, "Ret"),

desc_row(ea_data$earn_surp, "X")

)

desc_tabl$N <- nrow(ea_data)

desc_tabl$Firms <- max(ea_data$firm_id)

write_csv(desc_tabl, "../out/results/tab1-panA.csv")

desc_tabl|>

mutate(across(where(is.numeric), round, 4)) |>

kable()

| var | mean | sd | q5 | q25 | q50 | q75 | q95 | N | Firms | |

|---|---|---|---|---|---|---|---|---|---|---|

| 5% | Ret | 0.0044 | 0.0779 | -0.1252 | -0.0394 | 0.0027 | 0.0470 | 0.1392 | 67360 | 2966 |

| 5%1 | X | 0.0000 | 0.0044 | -0.0075 | -0.0005 | 0.0003 | 0.0014 | 0.0056 | 67360 | 2966 |

3. OLS estimates

3.1 Pooled OLS estimates

Just to have a frame of reference, here is the pooled ERC estimate

pooled <- ols_erc(ea_data)

kable(pooled)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| (Intercept) | 0.000000 | 0.0002955 | 0.00000 | 1 |

| earn_surp_dm | 3.116373 | 0.0665200 | 46.84867 | 0 |

3.2 Firm-level OLS estimates

Next, we nest the data by firm (ticker) and fit OLS ERC models by firm

nested_data <-

ea_data %>%

add_count(ticker, name = "n_EAs") %>%

nest(data = -c(ticker, n_EAs, firm_id)) %>%

mutate(ols_result = map(.x = data, .f = ~ols_erc(.)))

summary(nested_data$n_EAs)

Min. 1st Qu. Median Mean 3rd Qu. Max.

1.00 4.00 13.00 22.71 33.00 122.00 This is the distribution of firm-level ERC estimates

summary(ols_results$estimate)

Min. 1st Qu. Median Mean 3rd Qu. Max. NA's

-5034.136 0.068 3.884 6.041 10.650 5462.750 294 3.3 By-year OLS estimates

This is for the comparison in Figure 5.

byyear_data <-

ea_data_time %>%

nest(data = -c(year_id, EAYear)) %>%

mutate(ols_result = map(.x = data, .f = ~ols_erc(.)))

byyear_results <-

byyear_data %>%

select(-data) %>%

unnest(ols_result) %>%

filter(term == "earn_surp_dm")

4. Bayesian model with weakly informative priors

4.1 Model fitting

To fit a Bayesian model I use Stan, or, more precisely, its R bindings in cmdstanr. To fit a Bayesian model, we need to:

- Write the corresponding model using the Stan language

- Compile the code into a Stan model executable (an .exe file)

- Make a list of data to feed into the .exe file

- Let the model run and generate MCMC chains (or whatever algorithm is specified)

The model itself is coded in the Stan language. There are many excellent tutorials on Stan available online. So I won’t waste space explaining it here. For various reasons (e.g., debugging) it is customary to put the model code in a separate .stan file. All the model files can be found in the /Stan/ folder of the repo.

cat(read_lines("../Stan/erc-wkinfo-priors.stan"), sep = "\n")

data{

int<lower=1> N; // num obs

int<lower=1> J; // num groups

int<lower=1> K; // num coefficients

int<lower=1, upper=J> GroupID[N]; // GroupID for obs, e.g. FirmID or Industry-YearID

vector[N] y; // Response

matrix[N, K] x; // Predictors (incl. Intercept)

}

parameters{

matrix[K, J] z; // standard normal sampler

cholesky_factor_corr[K] L_Omega; // hypprior coefficient correlation

vector<lower=0>[K] tau; // hypprior coefficient scales

vector[K] mu_b; // hypprior mean coefficients

real<lower=0> sigma; // error-term scale

}

transformed parameters{

matrix[J, K] b; // coefficient vector

// The multivariate non-centered version:

b = (rep_matrix(mu_b, J) + diag_pre_multiply(tau,L_Omega) * z)';

}

model{

to_vector(z) ~ normal(0, 1);

L_Omega ~ lkj_corr_cholesky(2);

mu_b[1] ~ normal(0, 0.1);

mu_b[2] ~ normal(0, 40);

sigma ~ exponential(1.0 / 0.08); // exp: 0.08 (std (abnormal returns))

tau[1] ~ exponential(1.0 / 0.1); // exp: 0.1

tau[2] ~ exponential(1.0 / 40); // exp: 40

y ~ normal(rows_dot_product(b[GroupID] , x), sigma);

}

// generated quantities {

// array[N] real y_pred = normal_rng(rows_dot_product(b[GroupID] , x), sigma);

// }Next, we compile the model to an .exe file

model_wkinfo_priors <- cmdstan_model("../Stan/erc-wkinfo-priors.stan")

Now, we prepare the list of data to feed into the model.

input_data <- list(

N = nrow(ea_data),

J = max(ea_data$firm_id),

K = 2,

GroupID = ea_data$firm_id,

y = ea_data$AbEvRet,

x = as.matrix(data.frame(int = 1, esurp = ea_data$earn_surp))

)

We run the model

Beware, this fit can take a long time

fit_wkinfo_priors <- model_wkinfo_priors$sample(

data = input_data,

iter_sampling = 1000,

iter_warmup = 1000,

chains = 4,

parallel_chains = 4,

seed = 1234,

refresh = 1000

)

Running MCMC with 4 parallel chains...

Chain 1 Iteration: 1 / 2000 [ 0%] (Warmup)

Chain 2 Iteration: 1 / 2000 [ 0%] (Warmup)

Chain 3 Iteration: 1 / 2000 [ 0%] (Warmup)

Chain 4 Iteration: 1 / 2000 [ 0%] (Warmup)

Chain 1 Iteration: 1000 / 2000 [ 50%] (Warmup)

Chain 1 Iteration: 1001 / 2000 [ 50%] (Sampling)

Chain 4 Iteration: 1000 / 2000 [ 50%] (Warmup)

Chain 4 Iteration: 1001 / 2000 [ 50%] (Sampling)

Chain 2 Iteration: 1000 / 2000 [ 50%] (Warmup)

Chain 2 Iteration: 1001 / 2000 [ 50%] (Sampling)

Chain 3 Iteration: 1000 / 2000 [ 50%] (Warmup)

Chain 3 Iteration: 1001 / 2000 [ 50%] (Sampling)

Chain 3 Iteration: 2000 / 2000 [100%] (Sampling)

Chain 3 finished in 1941.6 seconds.

Chain 4 Iteration: 2000 / 2000 [100%] (Sampling)

Chain 4 finished in 1962.7 seconds.

Chain 1 Iteration: 2000 / 2000 [100%] (Sampling)

Chain 1 finished in 2088.8 seconds.

Chain 2 Iteration: 2000 / 2000 [100%] (Sampling)

Chain 2 finished in 2132.0 seconds.

All 4 chains finished successfully.

Mean chain execution time: 2031.3 seconds.

Total execution time: 2132.6 seconds.4.2 Summary of the posterior for selected parameters

Here is the summary of the resulting posterior distribution of the model parameters

fit_wkinfo_priors$summary(variables = c("mu_b", "sigma", "tau", "L_Omega[2,1]")) |>

mutate(across(where(is.numeric), round, 3)) |>

kable()

| variable | mean | median | sd | mad | q5 | q95 | rhat | ess_bulk | ess_tail |

|---|---|---|---|---|---|---|---|---|---|

| mu_b[1] | 0.004 | 0.004 | 0.000 | 0.000 | 0.003 | 0.004 | 1.000 | 3943.605 | 3333.804 |

| mu_b[2] | 3.669 | 3.668 | 0.107 | 0.108 | 3.490 | 3.850 | 1.001 | 2575.785 | 2404.202 |

| sigma | 0.076 | 0.076 | 0.000 | 0.000 | 0.075 | 0.076 | 1.003 | 4585.697 | 2582.434 |

| tau[1] | 0.006 | 0.006 | 0.001 | 0.001 | 0.005 | 0.007 | 1.000 | 1037.872 | 2015.912 |

| tau[2] | 2.804 | 2.802 | 0.125 | 0.125 | 2.600 | 3.008 | 1.002 | 1347.643 | 2243.416 |

| L_Omega[2,1] | -0.020 | -0.024 | 0.088 | 0.086 | -0.161 | 0.130 | 1.011 | 276.749 | 683.598 |

4.3 Comparing Bayesian ERC estimates to OLS estimates

To do this we need to extract the posterior draws for the ERC coefficients

posterior_b <- summarise_draws(fit_wkinfo_priors$draws(c("b")),

posterior_mean = mean,

posterior_sd = sd,

~quantile2(., probs = c(0.05, 0.25, 0.75, 0.95))

)

write_csv(posterior_b, "../out/results/fit_wkinfo_bi.csv")

posterior_erc <-

posterior_b |>

filter(str_detect(variable, ",2\\]"))

Code for Tab. 1, Panel C

tab1.C <-

rbind(

desc_row(posterior_erc$posterior_mean, "post_mean"),

desc_row(with(posterior_erc, q95 - q5), "post90_width"),

desc_row(with(ols_results, estimate[is.na(estimate) == FALSE]), "OLS"),

desc_row(with(ols_results, p.value[is.na(p.value) == FALSE]), "OLS pval")

)

write_csv(tab1.C, "../out/results/tab1-panC.csv")

tab1.C |>

mutate(across(where(is.numeric), round, 3))

var mean sd q5 q25 q50 q75 q95

5% post_mean 3.672 1.414 1.292 2.970 3.676 4.288 6.105

5%1 post90_width 7.837 1.440 4.946 6.933 8.314 9.013 9.345

5%2 OLS 6.041 178.593 -18.689 0.068 3.884 10.650 45.904

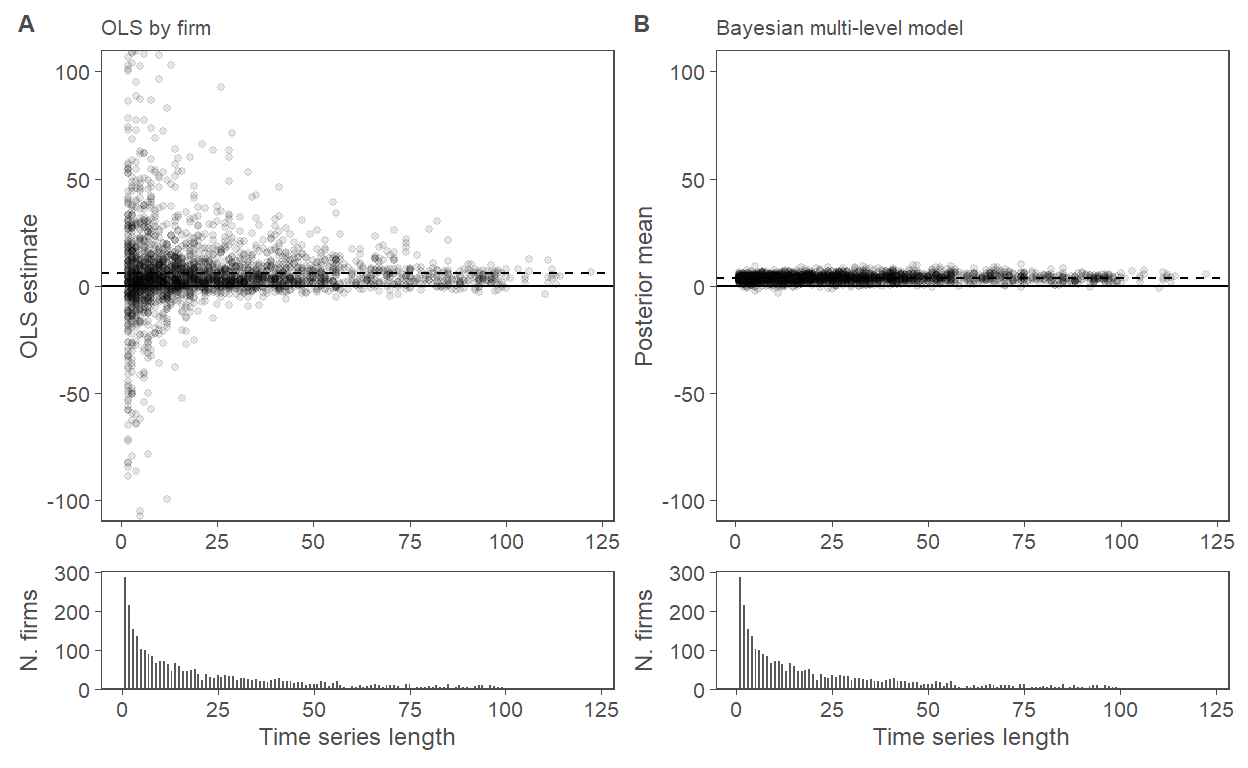

5%3 OLS pval 0.362 0.309 0.002 0.068 0.301 0.611 0.9274.4 Figure 4

graph_data <-

ols_results %>%

mutate(

post_mean = posterior_erc$posterior_mean,

post_sd = posterior_erc$posterior_sd

)

y_range <- c(-100, 100)

f4.panA <-

graph_data %>%

ggplot(aes(x = n_EAs, y = estimate)) +

geom_point(alpha = 0.1, size = 1) + # , width = 0.25) +

geom_hline(yintercept = c(0)) +

geom_hline(yintercept = mean(graph_data$estimate, na.rm = TRUE), linetype = "dashed") +

labs(

y = "OLS estimate",

x = NULL, # "Nr of Quarters in firm's time series",

subtitle = "OLS by firm"

) +

coord_cartesian(ylim = y_range)

f4.panB <-

graph_data %>%

ggplot(aes(x = n_EAs, y = post_mean)) +

geom_point(alpha = 0.1, size = 1) + # , width = 0.25) +

geom_hline(yintercept = c(0)) +

geom_hline(yintercept = mean(graph_data$post_mean), linetype = "dashed") +

labs(

y = "Posterior mean",

x = NULL,

subtitle = "Bayesian multi-level model"

) +

coord_cartesian(ylim = y_range)

f4.panC <-

graph_data %>%

ggplot(aes(x = n_EAs)) +

geom_bar(width = 0.5) +

scale_y_continuous(expand = expansion(mult = c(0, 0.05))) +

labs(

x = "Time series length",

y = "N. firms"

)

fig4 <-

f4.panA + f4.panB + f4.panC + f4.panC +

plot_layout(ncol = 2, heights = c(2, 0.5)) +

plot_annotation(tag_levels = list(c("A", "B", NULL, NULL))) &

theme(legend.position = "none")

fig4

Saving figure

save_fig(fig4, figname = "fig4", w = 6.2, h = 3.4)

5. Bayesian model with AR1 time trend

5.1 Model fitting

cat(read_lines("../Stan/erc-wkinfo-priors-time-pers.stan"), sep = "\n")

data{

int<lower=1> N; // num obs

int<lower=1> J; // num groups

int<lower=1> K; // num coefficients

int<lower=1> M; // num periods

int<lower=1, upper=J> GroupID[N]; // GroupID for obs, e.g. FirmID or Industry-YearID

int<lower=1, upper=M> TimeID[N]; // GroupID for obs, e.g. FirmID or Industry-YearID

vector[N] y; // Response

vector[N] x; // Predictor (without Intercept)

}

parameters{

matrix[K, J] z; // standard normal sampler

cholesky_factor_corr[K] L_Omega; // hypprior coefficient correlation

vector<lower=0>[K] tau; // hypprior coefficient scales

real<lower=0> sigma; // error-term scale

real mu_0;

real<lower=0,upper=1> rho_raw; // used to construct rho, the AR(1) coefficient

real<lower=0> sig_t; // error-term scale

vector[M] z_t;

}

transformed parameters{

matrix[J, K] b_i; // firm-level components

vector[K] mu_b; // hypprior mean firm-level coefficients

// The multivariate non-centered version:

mu_b[1] = mu_0;

mu_b[2] = 0;

b_i = (rep_matrix(mu_b, J) + diag_pre_multiply(tau,L_Omega) * z)';

// non-centered parameterization of AR(1) process priors

real rho = 2 * rho_raw - 1; // ensures that rho is between -1 and 1

vector[M] b_t = sig_t * z_t; // all of them share this term

b_t[1] /= sqrt(1 - rho^2); // mo[1] = mo[1] / sqrt(1 - rho^2)

for (m in 2:M) {

b_t[m] += rho * b_t[m-1]; // mo[m] = mo[m] + rho * mo[m-1];

}

}

model{

to_vector(z) ~ normal(0, 1);

z_t ~ normal(0, 1);

L_Omega ~ lkj_corr_cholesky(2);

mu_0 ~ normal(0, 0.1);

rho_raw ~ beta(10, 5);

sigma ~ exponential(1.0 / 0.08); // exp: 0.08 (std (abnormal returns))

tau[1] ~ exponential(1.0 / 0.1); // exp: 0.1

tau[2] ~ exponential(1.0 / 40); // exp: 40

sig_t ~ exponential(1.0 / 40); // exp: 40

vector[N] n_loc = b_i[GroupID, 1] + (b_t[TimeID] + b_i[GroupID, 2]) .* x;

y ~ normal(n_loc, sigma);

}model_wkinfo_timepers <- cmdstan_model("../Stan/erc-wkinfo-priors-time-pers.stan")

Again beware, this fit can take a long time

fit_wkinfo_timepers <- model_wkinfo_timepers$sample(

data = input_data2,

iter_sampling = 1000,

iter_warmup = 1000,

chains = 4,

parallel_chains = 4,

seed = 1234,

refresh = 1000

)

Running MCMC with 4 parallel chains...

Chain 2 Iteration: 1 / 2000 [ 0%] (Warmup)

Chain 4 Iteration: 1 / 2000 [ 0%] (Warmup)

Chain 1 Iteration: 1 / 2000 [ 0%] (Warmup)

Chain 3 Iteration: 1 / 2000 [ 0%] (Warmup)

Chain 3 Iteration: 1000 / 2000 [ 50%] (Warmup)

Chain 3 Iteration: 1001 / 2000 [ 50%] (Sampling)

Chain 2 Iteration: 1000 / 2000 [ 50%] (Warmup)

Chain 2 Iteration: 1001 / 2000 [ 50%] (Sampling)

Chain 1 Iteration: 1000 / 2000 [ 50%] (Warmup)

Chain 1 Iteration: 1001 / 2000 [ 50%] (Sampling)

Chain 4 Iteration: 1000 / 2000 [ 50%] (Warmup)

Chain 4 Iteration: 1001 / 2000 [ 50%] (Sampling)

Chain 3 Iteration: 2000 / 2000 [100%] (Sampling)

Chain 3 finished in 2301.3 seconds.

Chain 1 Iteration: 2000 / 2000 [100%] (Sampling)

Chain 1 finished in 2386.3 seconds.

Chain 2 Iteration: 2000 / 2000 [100%] (Sampling)

Chain 2 finished in 2400.0 seconds.

Chain 4 Iteration: 2000 / 2000 [100%] (Sampling)

Chain 4 finished in 2537.5 seconds.

All 4 chains finished successfully.

Mean chain execution time: 2406.3 seconds.

Total execution time: 2538.0 seconds.5.2 Summary of the posterior for selected parameters

Here is the summary of the resulting posterior distribution of the model parameters

fit_wkinfo_timepers$summary(variables = c("mu_b[1]", "sigma", "tau", "b_t",

"rho", "sig_t", "L_Omega[2,1]")) |>

mutate(across(where(is.numeric), round, 3)) |>

kable()

| variable | mean | median | sd | mad | q5 | q95 | rhat | ess_bulk | ess_tail |

|---|---|---|---|---|---|---|---|---|---|

| mu_b[1] | 0.003 | 0.003 | 0.000 | 0.000 | 0.003 | 0.004 | 1.004 | 4608.601 | 3102.494 |

| sigma | 0.075 | 0.075 | 0.000 | 0.000 | 0.075 | 0.076 | 1.000 | 3703.130 | 2184.654 |

| tau[1] | 0.006 | 0.006 | 0.001 | 0.001 | 0.005 | 0.007 | 1.001 | 1072.303 | 1881.667 |

| tau[2] | 2.615 | 2.612 | 0.122 | 0.118 | 2.419 | 2.821 | 1.005 | 1547.561 | 2254.383 |

| b_t[1] | 1.798 | 1.794 | 0.335 | 0.335 | 1.254 | 2.349 | 1.000 | 6564.086 | 3714.573 |

| b_t[2] | 1.699 | 1.701 | 0.310 | 0.319 | 1.183 | 2.198 | 1.000 | 5728.963 | 3821.598 |

| b_t[3] | 1.967 | 1.971 | 0.299 | 0.298 | 1.491 | 2.462 | 1.000 | 6325.139 | 3566.423 |

| b_t[4] | 2.302 | 2.300 | 0.319 | 0.318 | 1.783 | 2.843 | 1.001 | 5648.104 | 3809.811 |

| b_t[5] | 2.479 | 2.488 | 0.353 | 0.344 | 1.891 | 3.061 | 1.001 | 6555.830 | 3578.803 |

| b_t[6] | 1.969 | 1.971 | 0.326 | 0.333 | 1.424 | 2.495 | 1.000 | 5906.941 | 3710.413 |

| b_t[7] | 2.581 | 2.577 | 0.341 | 0.330 | 2.021 | 3.159 | 1.000 | 5834.040 | 3507.401 |

| b_t[8] | 3.065 | 3.070 | 0.351 | 0.356 | 2.490 | 3.641 | 1.001 | 5946.883 | 3773.475 |

| b_t[9] | 3.043 | 3.039 | 0.346 | 0.336 | 2.482 | 3.622 | 1.000 | 6807.729 | 2933.874 |

| b_t[10] | 2.824 | 2.826 | 0.348 | 0.348 | 2.242 | 3.382 | 1.000 | 6918.646 | 3719.018 |

| b_t[11] | 3.135 | 3.140 | 0.384 | 0.381 | 2.503 | 3.762 | 1.000 | 7432.118 | 3579.078 |

| b_t[12] | 3.175 | 3.176 | 0.383 | 0.392 | 2.540 | 3.799 | 1.001 | 6264.057 | 3811.178 |

| b_t[13] | 3.523 | 3.525 | 0.368 | 0.370 | 2.914 | 4.133 | 0.999 | 6556.955 | 3728.211 |

| b_t[14] | 3.838 | 3.837 | 0.398 | 0.398 | 3.180 | 4.476 | 0.999 | 6121.546 | 3726.720 |

| b_t[15] | 4.461 | 4.459 | 0.409 | 0.406 | 3.788 | 5.148 | 1.000 | 6665.553 | 3867.688 |

| b_t[16] | 5.957 | 5.956 | 0.403 | 0.402 | 5.299 | 6.633 | 1.000 | 5896.254 | 3454.660 |

| b_t[17] | 5.868 | 5.873 | 0.382 | 0.391 | 5.255 | 6.487 | 1.000 | 5911.323 | 3872.781 |

| b_t[18] | 6.461 | 6.453 | 0.394 | 0.397 | 5.827 | 7.104 | 1.001 | 5171.089 | 3228.712 |

| b_t[19] | 4.977 | 4.976 | 0.311 | 0.312 | 4.472 | 5.495 | 1.000 | 5879.135 | 3677.540 |

| b_t[20] | 4.169 | 4.168 | 0.265 | 0.265 | 3.724 | 4.605 | 1.000 | 5316.392 | 3666.933 |

| b_t[21] | 4.704 | 4.693 | 0.310 | 0.307 | 4.197 | 5.218 | 1.002 | 6076.813 | 3584.917 |

| b_t[22] | 5.870 | 5.866 | 0.358 | 0.362 | 5.289 | 6.451 | 1.000 | 5298.588 | 3418.853 |

| b_t[23] | 5.561 | 5.566 | 0.389 | 0.392 | 4.917 | 6.199 | 1.002 | 6182.931 | 3860.695 |

| b_t[24] | 4.562 | 4.567 | 0.441 | 0.446 | 3.835 | 5.281 | 1.000 | 5299.736 | 3824.800 |

| b_t[25] | 5.096 | 5.094 | 0.442 | 0.442 | 4.377 | 5.835 | 1.001 | 5638.985 | 3851.835 |

| b_t[26] | 5.659 | 5.664 | 0.444 | 0.446 | 4.944 | 6.378 | 1.000 | 7011.250 | 3646.906 |

| b_t[27] | 5.719 | 5.716 | 0.488 | 0.479 | 4.920 | 6.516 | 1.002 | 6129.497 | 3780.013 |

| b_t[28] | 6.448 | 6.438 | 0.612 | 0.603 | 5.446 | 7.467 | 1.001 | 6038.999 | 3444.120 |

| b_t[29] | 5.667 | 5.654 | 0.604 | 0.610 | 4.678 | 6.646 | 1.001 | 5950.123 | 3377.044 |

| b_t[30] | 4.365 | 4.346 | 0.601 | 0.607 | 3.415 | 5.365 | 1.000 | 5965.089 | 3543.557 |

| b_t[31] | 1.624 | 1.622 | 0.600 | 0.591 | 0.644 | 2.604 | 1.000 | 4175.004 | 3838.545 |

| rho | 0.894 | 0.898 | 0.037 | 0.035 | 0.828 | 0.948 | 1.000 | 2739.444 | 2701.058 |

| sig_t | 1.077 | 1.057 | 0.196 | 0.185 | 0.794 | 1.430 | 1.001 | 1669.068 | 2703.365 |

| L_Omega[2,1] | 0.133 | 0.131 | 0.093 | 0.091 | -0.021 | 0.292 | 1.007 | 382.611 | 631.552 |

Saving output for Panel E of Tab. 1

5.3 Comparing Bayesian ERC estimates to OLS estimates

posterior_b2 <- summarise_draws(fit_wkinfo_timepers$draws(c("b_i")),

posterior_mean = mean,

posterior_sd = sd,

~quantile2(., probs = c(0.05, 0.25, 0.75, 0.95))

)

posterior_erc2 <-

posterior_b2 |>

filter(str_detect(variable, ",2\\]"))

posterior_bt2 <- summarise_draws(fit_wkinfo_timepers$draws(c("b_t")),

posterior_mean = mean,

posterior_sd = sd,

~quantile2(., probs = c(0.05, 0.25, 0.75, 0.95))

)

write_csv(posterior_bt2, "../out/results/fit_wkinfo_time_bt.csv")

write_csv(posterior_b2, "../out/results/fit_wkinfo_time_bi.csv")

fit_comparison2 <-

rbind(

desc_row(posterior_erc2$posterior_mean, "post_mean"),

desc_row(with(posterior_erc2, q95 - q5), "post90_width"),

desc_row(with(ols_results, estimate[is.na(estimate) == FALSE]), "OLS")

)

write_csv(fit_comparison2, "../out/results/fit_comp-AR1.csv")

fit_comparison2 |>

mutate(across(where(is.numeric), round, 3)) |>

kable()

| var | mean | sd | q5 | q25 | q50 | q75 | q95 | |

|---|---|---|---|---|---|---|---|---|

| 5% | post_mean | 0.004 | 1.273 | -2.213 | -0.548 | 0.007 | 0.598 | 2.153 |

| 5%1 | post90_width | 7.410 | 1.259 | 4.847 | 6.664 | 7.835 | 8.413 | 8.733 |

| 5%2 | OLS | 6.041 | 178.593 | -18.689 | 0.068 | 3.884 | 10.650 | 45.904 |

Compare this to the numbers from the model without time trend

tab1.C |>

mutate(across(where(is.numeric), round, 3)) |>

kable()

| var | mean | sd | q5 | q25 | q50 | q75 | q95 | |

|---|---|---|---|---|---|---|---|---|

| 5% | post_mean | 3.672 | 1.414 | 1.292 | 2.970 | 3.676 | 4.288 | 6.105 |

| 5%1 | post90_width | 7.837 | 1.440 | 4.946 | 6.933 | 8.314 | 9.013 | 9.345 |

| 5%2 | OLS | 6.041 | 178.593 | -18.689 | 0.068 | 3.884 | 10.650 | 45.904 |

| 5%3 | OLS pval | 0.362 | 0.309 | 0.002 | 0.068 | 0.301 | 0.611 | 0.927 |

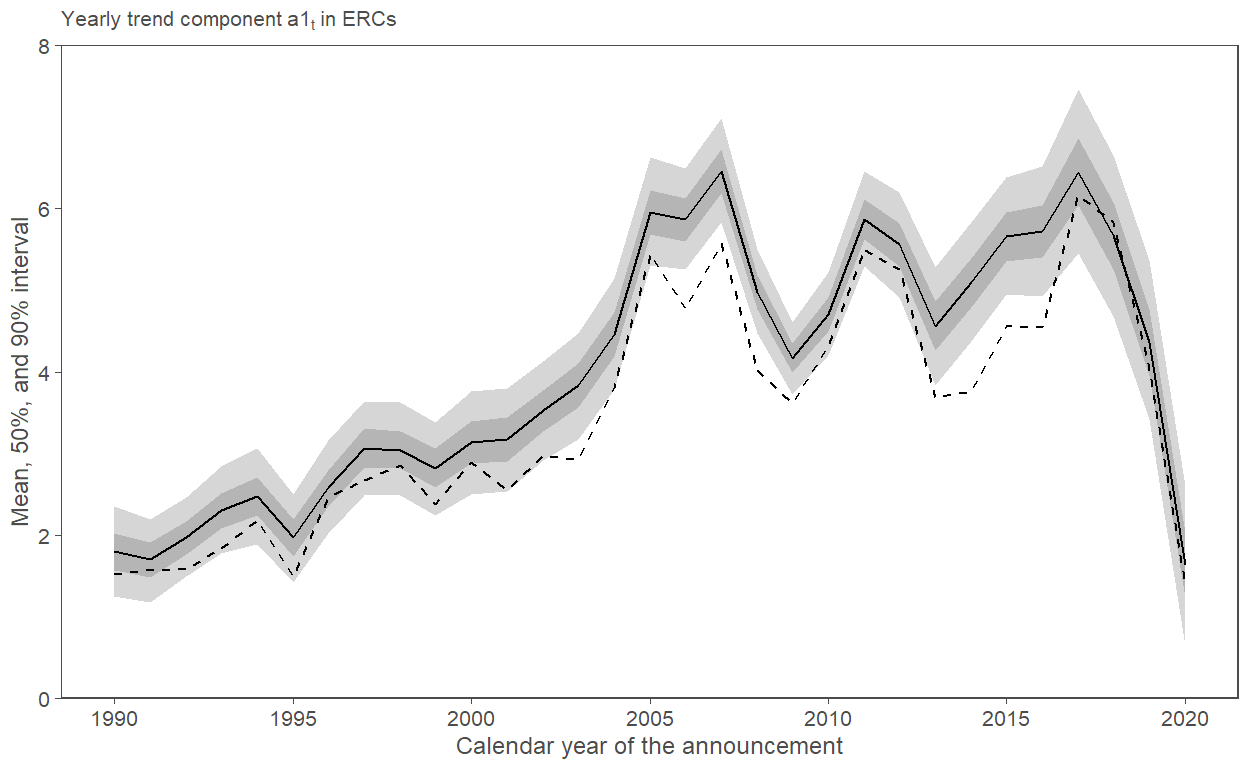

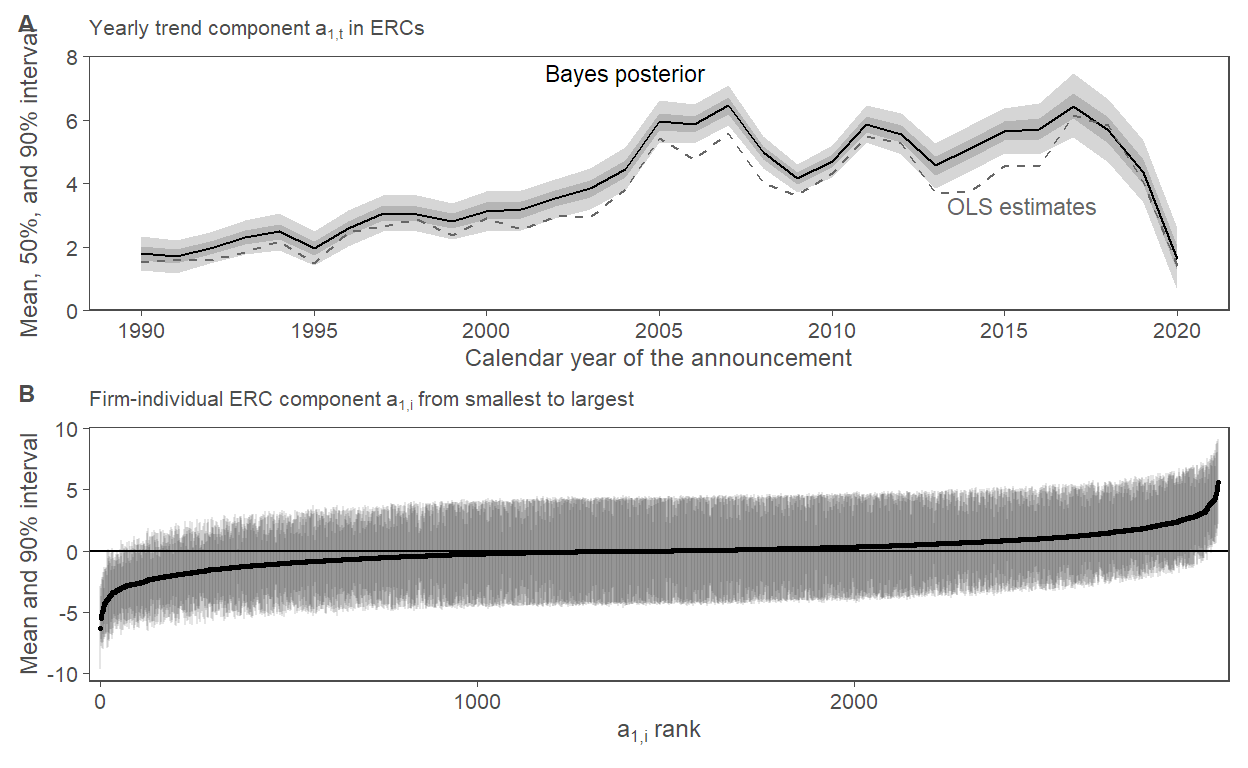

5.4 Fig. 5

posterior_bt2 |>

mutate(Year = 1:nrow(posterior_bt2) + 1989) |>

left_join(select(byyear_results, Year = EAYear, OLS = estimate),

by = c("Year")) |>

ggplot(aes(x = Year)) +

geom_ribbon(aes(ymin = q5, ymax = q95), alpha = 0.2) +

geom_ribbon(aes(ymin = q25, ymax = q75), alpha = 0.2) +

geom_line(aes(y = posterior_mean)) +

geom_line(aes(y = OLS), linetype = 2) +

scale_x_continuous(breaks = seq(1990, 2020, 5)) +

scale_y_continuous(limits = c(0, 8), expand = expansion(mult = c(0, 0))) +

labs(subtitle = expression("Yearly trend component"~a1[t]~"in ERCs"),

y = "Mean, 50%, and 90% interval",

x = "Calendar year of the announcement")

f5.panA <-

posterior_bt2 |>

mutate(Year = 1:nrow(posterior_bt2) + 1989) |>

left_join(select(byyear_results, Year = EAYear, OLS = estimate),

by = c("Year")) |>

ggplot(aes(x = Year)) +

geom_ribbon(aes(ymin = q5, ymax = q95), alpha = 0.2) +

geom_ribbon(aes(ymin = q25, ymax = q75), alpha = 0.2) +

geom_line(aes(y = posterior_mean)) +

geom_line(aes(y = OLS), linetype = 2, color = "grey40") +

scale_x_continuous(breaks = seq(1990, 2020, 5)) +

scale_y_continuous(limits = c(0, 8), expand = expansion(mult = c(0, 0))) +

labs(subtitle = expression("Yearly trend component"~a[1*","*t]~"in ERCs"),

y = "Mean, 50%, and 90% interval",

x = "Calendar year of the announcement") +

annotate("text", label = "OLS estimates", x = 2015.5, y = 3.3, size = 3, color = "grey40") +

annotate("text", label = "Bayes posterior", x = 2004, y = 7.5, size = 3)

f5.panB <-

posterior_erc2 |>

mutate(rank = rank(posterior_mean)) |>

ggplot(aes(x = rank, y = posterior_mean)) +

geom_hline(yintercept = 0) +

geom_linerange(aes(ymin = q5, ymax = q95), alpha = 0.1) +

geom_point(size = 0.5) +

scale_x_continuous(expand = expansion(mult = c(0.01, 0.01))) +

labs(y = "Mean and 90% interval",

x = expression(a[1*","*i]~"rank"),

subtitle = expression("Firm-individual ERC component"~a[1*","*i]~"from smallest to largest"))

fig5 <-

f5.panA / f5.panB +

plot_annotation(tag_levels = "A") &

theme(legend.position = "none")

fig5

Saving figure

save_fig(fig5, figname = "fig5", w = 6.2, h = 5)